It's Wednesday, and as usual I scout around various issues that I have been thinking…

Don’t mention the war! er the Troika …

“Don’t mention the war”! was a classic line from the episode – The Germans – in the comedy Fawlty Towers. Basil Fawlty implored his meagre staff to stay silent in case they offended some German tourists staying at his hotel. His attempt at self-censorship failed and led to hilarious consequences. I was reminded of the sketch (see it below) when I was reading the – Greek finance minister’s letter to the Eurogroup (February 24, 2015). Apparently, it is now a case of ‘Don’t mention the Troika’, ‘Don’t mention the Memorandum’ and never ever talk about the ‘Lenders’. The bullying threesome (European Commission, ECB and the IMF) are now known as “the institutions” and the “Memorandum” (the bailout package) is now to be called “The Agreement” and the “Lenders” have been recast as the “Partners”. Okay, and that is progress. The Reform package surely lets the Greeks choose which nasty policy they will implement but it is still nasty. Yes, it “buys them time”. The damage from massive unemployment and poverty eats into people every day. 4 months is a long time when you are on the street starving. And by the time this agreement is done – will the Germans be happy to unleash billions of euros via the European Investment Bank to allow the Greek government to continue running fiscal primary surpluses and keep pumping interest income on outstanding debt into ‘foreign’ coffers? Pigs might fly.

Two days ago, Eurostat published the latest inflation data for Europe – Annual inflation down to -0.6% in the euro area – and reported that:

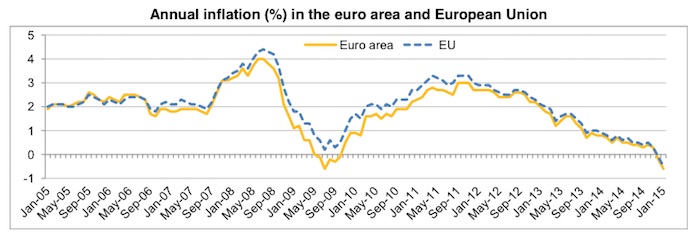

Euro area annual inflation was -0.6% in January 2015, down from -0.2% in December. This was the lowest rate recorded since July 2009 … negative annual rates were observed in twenty-three Member States. The lowest annual rates were registered in Greece (-2.8%) …

Greece is deflating at a monthly rate (January 2015) of 1.2 per cent – that is a dramatic negative inflation rate.

The following graph is taken from the Eurostat publication. It tells you that the ECB is now a total failure given that its charter is clearly specified in Article 127(1) of the Treaty on the Functioning of the European Union:

The primary objective of the European System of Central Banks … shall be to maintain price stability.

With deflation, prices are not stable and they have not been stable for some years. The deceleration, which preceded the deflation, began in September 2011.

The pace of deflation is now gaining speed.

Who is resigning from the ECB Board? Who is being sacked?

I know that I am an armchair observer. I know the Greek Finance Minister personally and he is very bright. I know that.

I know that the US economist, James Galbraith, who many mistakenly label as a proponent of Modern Monetary Theory (MMT), is in Athens and knows ‘inside stuff’ and assures us all is going to plan – see Reading The Greek Deal Correctly

He lectures those who would claim that the Greeks have surrendered again as being incorrect! Okay. We will see on that one.

There are several others – mostly ‘progressives’ – who are constructing the Reforms and the process to date in a positive light – almost as if they want to hang onto the thinnest thread of hope given how bleak the overall situation is.

Hope is good. But deception is bad.

One Syriza MP clearly believes that the Greek people are being sold out by his own party. I guess Alex Tsipras and the Finance Minister “respect” the national Greek hero from World War II – Manolis Glezos – but don’t think much of what he has to say.

Glezos was the person who was in the Greek resistance against the Nazis during the World War II occupation. Together with another resistance member he tore the swastika flag down from the Acropolis on May 20, 1941, which was a famous historical act that inspired broader resistance.

He has a history of travail and imprisonment in the face of oppression – first the Nazis, then against the right-wingers during the – Greek Civil War, and then during the Cold War.

He is now a Syriza Parliamentary Member and has written in Monthly Review (February 22, 2015) – Before It Is Too Late – that the Greek peope voted on January 25, 2015 for “what SYRIZA promised”.

He said it was unambiguous:

We will overthrow the regime of austerity that is not only the strategy of the oligarchy in Germany and other EU creditor states, but also the Greek oligarchy.

We will get rid of the Memoranda and the Troika and repeal all the austerity laws. The day after the elections, with one law we will overthrow the Troika and overturn its consequences.

The developments to date have clearly not honoured those pledges.

Glezos then said:

For my part, I apologize to the Greek people because I, too, was a collaborator in the creation of this illusion.

The EUObserver reported (February , 2015) – Greece tables reforms, awaits eurozone approval – that:

Tsipras’ spokesman said that Glezos is “someone whom we will never cease to honour,” but that his comments were “misguided and wrong”.

Glezos clearly understands external oppression and he is right to say that the whole Eurozone arrangements with the Eurogroup as one of the central enforcing groups is an oppressive regime. There are no guns involved but the oppression and the undermining of democracy and national sovereignty is real.

It is invasion and occupation by another means.

In April last year, the – Employment and Social Affairs Committee (EMPL) – of the European Parliament released its – ECON evaluation of Troika.

You will note they don’t mess around with “The Institutions”. They conducted their – Troika inquiry – into the way that the Troika’s actions affected Cyprus, Greece, Portugal and Ireland.

I guess they might have to cut and paste “The Institutions” in everywhere now to conform with the latest madness.

The Report discussed in the European Parliament in the March 2014 plenary:

… calls on the Troika and the Member States concerned to end the programmes as soon as possible and to put in place crisis management mechanisms …

that expectations of a return to growth and job creation through internal devaluation, in order to regain competitiveness, have not been fulfilled … [as a result of the Troika’s] … tendency to underestimate the structural character of the crisis as well as the importance of maintaining domestic demand, investment and credit support to the real economy.

Why would anyone want to go along with the Troika for a single extra day?

Galbraith, writing on February 23, 2015, answers that it is a “poisoned chalice” anyway.

He also lectured critics for assuming that the “loan agreement” would be terminated, despite Syriza making this a central part of their electoral platform. They got their mandate in no small part because of that pledge as Manolis Glezos tells us.

Galbraith claims we are stupid for thinking that the loan agreement would go because:

… there was never any chance for a loan agreement that would have wholly freed Greece’s hands.

Insider-stuff! So Syriza tells the people one thing but always knew another. Is that it? Okay, if so, then we have no way of knowing what is going on really nor do the Greek people.

He went on to articulate the point:

The only choices were an agreement with conditions, or no agreement and no conditions. The choice had to be made by February 28, beyond which date ECB support for the Greek banks would end. No agreement would have meant capital controls, or else bank failures, debt default, and early exit from the Euro. SYRIZA was not elected to take Greece out of Europe. Hence, in order to meet electoral commitments, the relationship between Athens and Europe had to be “extended” in some way acceptable to both.

Galbraith is on the public record as supporting Greece staying the euro. I completely disagree with his rationalisation of that position.

Further, whether the ECB would end its funding of Greek banks is not something Galbraith actually knows from the basis of his ‘inside’ information. He is repeating assertion.

As I wrote in this blog – Greek bank deposit migration – another neo-liberal smokescreen – it would be an extraordinary act by the ECB if it allowed the entire Greek banking system to enter bankruptcy because it refused them the necessary reserves to satisfy the regular demands on the payments facilities.

The ECB does not have a legal charter to allow that to happen. Indeed, their charter requires them to maintain financial stability and that does not include, under any Troika-stretched imaginative definition, the deliberate bankrupting of an entire nation’s private banking system.

Further, it seems he thinks there was a priority of electoral commitments. The no exit trumps all and austerity continues.

I understand the problem. I wrote about it previously – Conceding to Greece opens the door for France and Italy and Greek elections – a solution doesn’t appear to be forthcoming and Greece – two alternative views.

It is clear that Syriza could not honour its end austerity pledges and still stay in the Eurozone. They should have been honest about that in the first place.

Sure enough, the Reform document was produced by the Greek government and not delivered to them by some Troika goon or another with a pen to sign on the dotted line.

Imagery is important and that is a change. They determine the nature of the austerity. With 25 per cent unemployment I don’t see that imagery as being a very good substitute for immediate and large-scale job creation.

The Reform document makes it clear that the Greek government will promise to undergo a raft of fairly generally (that is, unspecified) ‘structural’ changes but will stick within the fiscal straitjacket imposed by the Stability and Growth Pact and the Bailout requirements (with marginal changes).

The document says that the Greek government will:

Ensure that its fight against the humanitarian crisis has no negative fiscal effect.

What exactly is a “negative fiscal effect”. Well, for you etymologists, it is neo-liberal Groupthink speak for increasing the fiscal deficit.

We now think of rising fiscal deficits as a negative and increasing surpluses as positive irrespective of what is happening in the real economy to income growth and unemployment.

And then there is the rub – the Greek plan which includes a commitment to run a primary fiscal surplus this year of 1.5 per cent (that is, surplus net of interest income paid out) apparently is based on their belief that a massive fiscal stimulus is going to come from the European Investment Bank (EIB) which will end austerity by boosting growth and employment.

It is like a massive export income boost or a federal injection to a state.

Galbraith continued his lecture:

There is no money in Greece; the government is bankrupt. Large-scale Keynesian policies were never on the table as they would necessarily imply exit – an expansionary policy in a new currency, with all the usual dangers. Inside the Euro, investment funds have to come from better tax collection, or from the outside, including private investors and the European Investment Bank.

Which is true.

But the reforms offered and now agreed to are not conditional on any EIB activity. Trying to exploit different propensities to consume among different taxpaying cohorts is not going to provide sufficient spending capacity in Greece to dent the crisis much less solve it.

A massive fiscal intervention is needed even though we know that the potential growth path of the economy is significantly lower than it was pre-crisis.

It is clear that the Finance Minister supports an EIB fiscal stimulus. He was the co-author Stuart Holland of their so-called Modest Proposal.

One recalls Jonathan Swift’s satire of the same name, published in 1729, where Irish parents were encouraged to ease their economic travails by selling their children as food to provide culinary pleasure to the rich. The latest version (July 2013) was co-authored with James Galbraith.

The Modest Proposal is motivated by the assertion is that “a Eurozone breakup would destroy the European Union, except perhaps in name” which would pose a “global danger”. I disagree with those assertions and my forthcoming book tells you why.

You can read the book text as it was written in unedited form via this link – Euro Book. Search for ‘Modest Proposal’ for a full critique.

I do not consider an exit to be a disastrous option. For example, the Finance Minister wrote in 2012 a critique – Weisbrot and Krugman are Wrong: Greece cannot pull off an Argentina – who both advocated an exit.

One of his arguments was related to two two mythical Greeks Dimitri and Kiki who will shift their savings into offshore banks (in euros) in anticipation of the exit. They might also “stuff them in their mattresses or hide them in freezers”.

The Finance Minister wrote that:

This means that, by the time we come to an exit from the euro, the stock of savings will be in euros and the flow of incomes and pensions (once the banks re-open) will be in drachmas.

And the conclusion:

Moreover, the very availability of such large quantities of ‘hard’ currency savings, in the hands of the average Dimitri and Kiki on the street, will ensure that the decline in the value of the new drachma will be precipitous …

This is a common claim. That the currency will depreciate so much it will wipe out any real prosperity as a result of the devalued savings (expressed in drachma).

It have considered the claim that a new Greek currency would significantly depreciate against the euro once issued previously.

Why would that happen? Foreign exchange parities are determined by supply and demand.

Who would be issuing the new Drachma? Answer: Only one institution – the Greek government via the central bank.

What is the current volume (supply) of new Drachma in the foreign exchange markets? Answer: zero – it doesn’t exist.

If the Greek government restricted its supply but were able to require people to demand it – to pay taxes etc – then why would the currency depreciate violently in the period after issue?

You are thinking (like most people) of an existing tradable currency that is unpegged or something like that. Then the depreciation can be sudden because there is a lot of supply.

A significant exchange rate depreciation of the new drachma in the short-term given the fact that supply would be limited. The examples often used, such as Iceland and Argentina, all relate to currencies that were already supplied in volumes to the foreign exchange markets.

The basic conclusion is that it is hard to see how a proposal that involves no fiscal transfers or changes to the Treaty can provide a lasting solution to the mess.

The modesty of the proposal is its shortcoming. It will not solve the inherent problems within the Eurozone, which are defined by the very political constraints that the authors recognise force them to adopt these ‘modest’ proposals, in lieu of more effective and lasting solutions.

The political constraints they identify include those that prevent the ECB from funding governments directly, the inability to issue euro-bonds, the impasse over the creation of a “properly functioning federal transfer union” (p.3); and the time delays that would be involved in activating any Treaty changes, once agreed.

One element of the proposal was sensible.

They promote a large-scale, European-wide “Investment-led Recovery and Convergence Programme” (IRCP). It is one of the few proposals of the many that have emerged in the literature that explicitly seeks to reverse the austerity mindset by increasing total spending and, as a consequence, directly addresses the core short-run problem of stagnant growth

The argument that substantial new investment could kick-start growth if put into productive use, is sound. It mimics the emergency responses that marked the New Deal in the US between 1933 and 1937.

The questions are whether the scale of the program would be sufficient to generate a recovery, given how large the output gaps are at present, and whether a massive investment program could be absorbed without creating damaging imbalances.

Juncker’s plan is so small in scale that it will not do the trick. And Germany will not agree to any larger Eurobonds-type scheme.

The authors merely assert that the scale of the program would be sufficient. If Germany is excluded, real GDP in 2013 for the remaining Eurozone nations was some 4 per cent below its 2007 level (some 253 billion euros).

Similarly, investment was about 27 per cent lower. Even assuming a very generous spending multiplier, the injection that would be required to make up that gap would dwarf the previous allocations that the EIB has handled.

Further, investment has a dual characteristic – it adds to spending in the current period but also to the supply capacity of the economy in the subsequent periods. Would the growth in consumption spending pick up quickly enough to absorb the new capacity?

While the authors have characterised their proposal as akin to the New Deal (see Varoufakis et. al., 2013), it should be remembered that the US program was heavily weighted towards providing relief to unemployed and impoverished citizens in the form of cash payments and direct public sector job creation.

This sort of relief is outside of the ambit of the ‘Modest Proposal’ and thus it is questionable whether an investment-led answer to the deficient total spending will generate the gains necessary to lift household consumption in say Greece, where in 2013, it was around 25 per cent below its 2007 value.

But the necessary funds that would be necessary to implement this external fiscal stimulus are not in the wind.

As I explained in this blog – Greece – two alternative views – Greece will not achieve growth with balanced fiscal positions.

How does the Party plan to fill the massive output gap that Greece has? Output gaps can only be closed by increasing output. That requires increased net public spending not balanced fiscal positions or even surpluses.

Purchasing power taken of the ‘rich tax evaders’ might be at the expense of saving but will still not deliver the required net boost

Greece has lost 25 per cent of its real GDP since 2008. While potential output has also surely declined (as firms have scrapped productive capital) in the face of a massive decline in the investment ratio, it remains there is a huge unused capacity in the country. The mass unemployment is testament to that.

While there might be good reasons for redistributing the existing fiscal outlays across the competing interests, the overwhelming fact is that the Greek public deficit has to rise substantially – by multiples of the current Stability and Growth Pact fiscal limits of 3 per cent.

Running a fiscally-neutral policy to help people will only partially stimulate overall spending in the nation. The reality is that Greece needs a public stimulus that is way beyond anything that is allowed under the current rules.

A balanced budget position doesn’t resolve that issue.

But the Greeks can fix that in a single decision – leave the Eurozone and restore currency sovereignty.

But that is off the agenda because the progressive left in Greece appear to have bought the line that the ‘European Project’ requires a monetary union and being in the Eurozone is a sign of sophistication and a break with the Colonels!

I have some sympathy for their fears that the early 1970s is not far in the past and that the military is being bought off with new military toys etc (imported from Germany no less) which have largely escaped the clutches of austerity.

The likelihood of a military coup if Syriza advocated leaving the Eurozone is something I cannot assess.

But the idea that Greece will return to some backwater if it is not part of the Eurozone is a delusion.

Conclusion

After several weeks since the election we are still not exactly clear what is happening.

But the only reasonable conclusion to date is that Syriza’s stated policy aims are not mutually consistent and that is why they have given significant ground to the Troika – er, The Institutions!

They cannot achieve the (motherhood) aspirations of higher growth and increased incomes and equity while allowing Brussels to dominate the magnitude of their fiscal deficits.

They cannot achieve their aims with a fixed exchange rate (effectively no independent exchange rate) with Germany as a partner in the monetary union.

Their policy pledges resonate with the suffering population. But the reality is that the population is not being educated by progressive forces about the self-inflicted damage that retaining the euro as their currency is causing.

Political parties that make it a root-and-branch commitment to remain in the Eurozone do not help.

Don’t mention the War

In case you have forgotten the sketch, here is Basil in all his goose-stepping glory after his continual mentions of “the War” had upset one of the German tourists.

British Green’s leader can’t say “we will increase the deficit”!

The UK Green’s leader gave an interview on the party’s housing policy, which was reported on ABC News today (February 26, 2015) – Natalie Bennett, leader of Britain’s Greens, apologises after struggling on party polices in ‘very bad’ interview.

She was asked how the Party would pay for the land necessary “to build 500,000 new social rental homes” and replied:

Right, well, that’s, erm, you’ve got a total cost, erm, that will be spelt out in our manifesto …

You can listen the interview via the ABC report. Cringe a while then think about the problem.

She could have simply said – “If we are in government, then the British people will understand we issue the currency and we will pay for this by increasing the deficit and instructing the Bank of England to credit the necessary bank accounts to facilitate the purchases.”

That is the plain truth of it.

They can do that. If there is a need for 1/2 million more social houses then they should do that as long as it is within the real economy’s capacity to provide the housing.

If it is not in the capacity then they would have to assess priorities and perhaps have to raise taxes to withdraw spending capacity from the private sector.

Simple macroeconomics.

The reason she stumbled is that the Greens are generally ‘neo-liberals on bikes’ and cannot bear to talk about deficits etc because they are constrained by the current orthodoxy.

The consequences of that are (a) no social housing will actually emerge; and (b) she sounds like an idiot when being interviewed.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

It would be good if YV could give his version of what’s going on.

Yet, despite previously writing:

“My plan is to defy such advice [to stop blogging]. To continue blogging here even though it is normally considered irresponsible for a Finance Minister to indulge in such crass forms of communication ”

he’s not updated his website, nor allowed any comments to appear, since the end of last month.

Bill,

The site inflation.eu gives the the Greek ANNUAL inflation rate for 2014 as -1.31 %.

You say, “Greece is deflating at a monthly rate (January 2015) of 1.2 per cent – that is a dramatic negative inflation rate.” Did you mean to say this or is the inflation rate you quoted actually for Feb 2013 to Jan 2014? That is to say, a running annual rate ending at the end of the month mentioned?

“If it is not in the capacity then they would have to assess priorities and perhaps have to raise taxes to withdraw spending capacity from the private sector.”

That’s perhaps something that MMT needs to address. You don’t necessarily need to use taxes, because taxes may not work and may not be specific enough to eliminate the required demand.

Get down to the real level and ask yourself what you are after – house builders to work on the social project and not other projects. You’re supply side limited because otherwise you wouldn’t be considering ‘making space’.

So there are other measures to ensuring that there isn’t an alternative bid for resources. One of those is simply banning the alternative bid – either temporarily or permanently. So you could suspend planning permission until you have sufficient house builders signed up to build the 500K houses at a price that is acceptable to government. Remove their alternative sources of employment until they deal.

The other is to restrict the supply of borrowed money, not by jiggling interest rates but by simply preventing the banks from issuing private mortgages to purchase new houses – again until sufficient house builders have signed up to build the 500K houses at the price that is acceptable to the government.

Of course simply the expectation of such a move is probably sufficient to get the house builders to deal. So they build the 500K houses to avoid disruption to their other activities.

House purchase is pretty unique admittedly. If people are prevented from buying new houses they are unlikely to borrow the money to buy yachts or cars. Yes they may bid up existing houses, but they would do that anyway since the problem is that you are supply side limited. However if you are building 500K new homes, then you are going to be taking away the private demand for 500K homes at the same time.

Another of the features of the neo-liberal era has been deregulation. Government banning things went out of fashion and everything had to be decided by price. However since price and value are clearly not the same thing, and government is about pursuing value for the public purpose I think judicious and sparing use of banning things is probably a better approach in some cases than jiggling taxes.

Bill,

I agree with you 100% on EU and Grexit. Greece must exit. For what it’s worth I would recommend the following. Of course, I am nobody and my opinions have no force. I have no Greek heritage either (other than at the broad Western culture level).

Greece should (under Syriza);

(1) Leave the EU, float its own currency and repudiate all foreign debt.

(2) Run large deficit budgets in its current deflationary depression.

(There is no doubt Greece is in a deflationary depression.

The unemployment rate = 27% and inflation rate = – 1.5%.)

(3) Implement minimum wage and pension rises.

(4) Increase the size and scope of its public services.

(5) Crack down on corruption and tax evasion with a larger police force and larger internal revenue service.

(6) Freeze, confiscate and nationalise the assets of the oligarchs.

(7) Cut back on military spending.

(8) Take pre-emptive steps to prevent a right-wing military coup.

…to the deficient total spending will generate the gains necessary to lift household consumption in say Greece, where in 2013, it was around 25 per cent below its 2007 value. …

I am a loss on that one. How can Greece’s household consumption by spending exist when the EU through the Troika demand nil basic tax allowance and multiple layer of taxes, however poor, on households and small to medium independent businesses?

Shops close in Athens and never re-open all around the centre of the city and around the Parliament. Even where the tourists teem. These shops were small inherited businesses from parents and grandparents and the sole means of jobs.

Also inherited, that had been gained free by family over generations since the War, were the equivalent of a

‘citizen income’ when there is practically no welfare help, of apartments and little houses for money from rents. This is why a property tax in Greece is so damagning to the poor, who own, on average, about 2 or 3 apartments in Athens beyond their own home.

It was the EU who demanded wage cuts not only in the public sector, but in the private sector who did not owe the national debt.

Was it not the EU who raised the retirement age throughout EU member states and then took from the pensions funds, even if they were not state run, and private works one, so even current pensioners, however old, had their pensions from all sources cut to the bone?

Without lifting the massive tax burden on the poor to average waged, no spending will happen in Greece, will it not?

Why should Greeks pay tax when all this tax money does not helps them individually in the least, and just flows abroad? No stimulus investment, no tax cuts to businesses and people and there has to be humanitarian help.

Greece’s collected taxes cannot bring about Roosevelt’s New Deal as Greece’s government owes debt plus massive interest.

[Bill edited out constant advertising for a UK pension cause – please do not continue to advertise on this site – comment is good, using the site to continually advance your own agenda is not]

Dear Bill

You said that the new drachma can’t devaluate. That’s a somewhat contrived argument. If the Greek government starts to issue the drachma again, it has to use a conversion rate. After all, the Greek government is now paying all its employees and imposing taxes in euros. If a civil servant who is currently paid 2500 euros a month will receive 2500 drachmas after the Grexit, then the implicit conversion rate set by the government is 1:1. Subsequently, it can go down.

A Grexit would enable the Greek government to stimulate the economy by running big deficits, but it can’t be denied that Greeks will suffer a welfare loss because of dearer imports caused by a devaluation. Also, many creditors will incur a loss if all contracts in Greece which currently are in euros are drachmatized.

Let’s say that a Grexit would result in a quick recovery of Greek GDP to the level 2008. That would be an increase of 25%, assuming that current GDP is 80% of what it was in 2008. If Greeks spend 30% of their income on imports and if those imports become dearer by 40%, then the welfare loss due to the devaluation will 8.6%, 30/1.4 = 21.4. If we subtract the 8.6% from the 25%, then the net welfare gain will still be 16.4%.

Regards. James

@petermartin2001

This blog reports a radio interview with YV.

https://greekanalyst.wordpress.com/2015/02/25/the-juicy-interview-of-greek-finance-minister-yannis-varoufakis/

Noticed on the Facebook thingy that the Greek socialists are making basic income noises.

Not sure if this is true but it sounded about right as they wanted to fund the project from the tax net !!!!!! rather then introduce new tokens.

This hybridisation and bastardization of sincere policies is a general characteristic of the socialists.

I am afraid the social creditors observation of this force was spot on – they are simply the most effective managers for the credit monopolists.

Which makes them far more dangerous a force.

Their superb ability to carry people over cliffs is quite astounding.

The objective is clearly to reduce running “costs” by eliminating social welfare civil servants jobs ( which in the current monetary ecosystem this “work” is needed to access purchasing power) and not distribution of income.

So we are witnessing dramatic efforts to increase efficiency while avoiding at all costs the distribution of the new surplus.

Let’s face it lads – Father Coughlain was right about FDR socialists,

Galbraith unlike some politicians cannot claim ignorance.

He knows exactly what he is doing.

Bill, glad to see we’re in good company on the collaboration issue!

😉

@

Warren

I woke up to you proper when I witnessed you giving a lecture about how the British banking system entrapped tribal Africans into their tax net,

If I remember correctly I think you found it highly amusing.

I guess we will now begin to hear sniping remarks about how Chesterton like characters are closet masonic Nazis rather then old wise men who simply wanted to bring back from the dead merry old England.

It is still understood in albeit declining Irish circles that Tudor England was the first fascist state.

I guess it was because we are the blackest white men in Europe.

The memory runs deep.

and its all happened before of course – not just in Ireland as dork alludes to above… in his very odd way. but in greece as well ..

excellent article from James Petras who advised the dark lord papendreau.. it almost lends credence to the idea that as soon as someone with a heart and a brain is elected they are taken into a room and cloned with an identical ‘they live’ style neoliberal alien monster.

http://www.thepeoplesvoice.org/TPV3/Voices.php/2015/02/21/the-assassination-of-greece

“If a civil servant who is currently paid 2500 euros a month will receive 2500 drachmas after the Grexit, then the implicit conversion rate set by the government is 1:1”

How can it go down at that point?

If you tax at a high level then there will be a demand for the drachma in excess of supply and people will *have to* repatriate Euros to purchase the drachma to pay the taxes. Those drachma may or may not be supplied by the central bank depending upon policy allowing it to set the rate where it wants it to be initially.

Where’s the selling demand in excess of the buying demand that make it go down in that scenario?

Once again you state a belief without explaining the mechanism and fall completely into the fixed exchange mentality. Floating exchange rates clear at the point supply and demand are equalised. FX is as near to a perfect market as you can have.

The currency is a public monopoly and that means monopoly rules apply.

Bill,

My take all along s that there will be an exit, and Syriza knows it, but they have to try to stay in anyway for 2 reasons:

1)It’s an election pledge

2)They need time to make the change to a “Greek Euro” or Drachma anyway.

Galbraith said above:

So could he mean a later exit is what will probably happen?

Okay, maybe i’m seeing what I want to see.

Kind Regards

Bill I wouldn’t count on the ECB not doing an extraordinary act — and remember it is up to the board of directors to decide if they are going to continue to provide liquidity, and that these are from the countries using the euro, and on a rotating basis — for voting that is.

I was wondering to if you might do a reprise of one of you December articles where you pointed out that Greece’s ‘growth’ was mostly due to the way the stats are produced, and maybe include Spain as well which it would appear is also deflating despite GDP growth, and note in articles such as this: http://fistfulofeuros.net/afoe/spains-good-deflation/

Because it would seem the German perspective, including from the likes of Der Spiegel, is that since this countries are having ‘growth’ they just need to stick with the program and that it is working.

Neil,

I think there would be some devaluation, say 15%, because the Greek government would not be able to have strong enough taxation whilst running a larger deficit. If for the first year Greece increased the deficit by just 5%GDP while the devaluation happens, it would simply push inflation up to about 2 or 3% which is fine. After the one off devaluation, they could continue running an even larger deficit until the output gap is closed.

While the devaluation is taking place, the Greek government should only issue debt (at a fixed rate) to those who want to buy it. Or if EU rules prohibit this (and I think they do), they can simply order the central bank to purchase large amounts of gov’t debt and hold the stock of debt until the end of time, returning the interest payments to the treasury.

Very basic, and probably stupid, question.

“No agreement would have meant capital controls,”

What is wrong with capital controls?

I know Iceland imposed them, and I read that they are anxious to get rid of them but not able to do so at present. So there must be something wrong with them. What is it ? I do not understand the problem, since “capital flight” is also characterised as a bad thing.

Presumably ideally you want no controls but a situation in which there is no will to remove capital from the country. I would like a unicorn, but it is not on offer. So in the absence of that ideal option it seems to me that the alternatives are capital controls which are determined by government; or capital flight, which is determined by the elite who hold the capital. If they are both bad then I prefer the one which is under the control of the elected body, unless there is a good reason why the other is better. Is there?

1. Greece is facing 2 separate short-term problems – low productive capacity utilisation and uneven distribution of income / wealth. Also – the productive capacities of the Greek economy didn’t look good even before the crisis. What exactly could they export – compared with Germany?

2. In theory the government can address low productive capacity utilisation even within the framework of using a foreign currency (EUR) as a legal tender – by engineering a balanced budget stimulus. Imagine (as an intellectual experiment) the Greek government paying extra EUR 1bln/month to hire 1 million unemployed (on top of their unemployed benefits everyone would earn EUR1000/month). But here is a trick. Immediately after getting paid, freshly employed workers will have their extra income confiscated. The marginal tax rate = 100%. OK this would constitute a kind of forced labour acquisition. This was very popular during the Stalinist period in the CCCP and satellite countries – they didn’t even bother to pay people. It existed in a rudimentary form even during the “real socialism” phase. When I was a school kid we were supposed to go and clean up leaves in the park in autumn (or pick up dogs poo) – in the name of “social works” – especially picking up the dogs poo was supposed to be an efficient method of embedding the principles of scientific communism into our minds.

EUR1bln/month is not a huge volume (flow) of money even in Greece. What about financing workers from extra wealth taxes? The marginal propensity to consume of Greek oligarchs is low and they have a lot of income to tap into. This would actually work if leaks are sealed off or compensated for.

3. The above could also help addressing the uneven income distribution issue and as a consequence drain some of the wealth from the oligarchs. Unless they oligarchs fight back. It is very unwise for YV not to have a lot of personal bodyguards. I have also noticed the “universal income” elements in the recent talk, too. This would be far less efficient in stimulating the economy as some of the extra income would be used for debt deleveraging.

4. I am still unsure whether there is no political gambit, something big has been promised to the Greeks or whether Galbraight was simply asked by his pals from the Obama administration to help avoiding Grexit at any cost during the critical phase of the conflict in the North Africa, Middle East and Ukraine. “Dont’s mention the war” – which war? Putin is threatening cutting off gas supplies and his tanks are ready to roll into Mariupol and possibly Kharkov. Ukrainian propaganda is saying that Kuchma the former President of Ukraine stated a few days ago that “We were actually given an ultimatum: If we don’t accept its terms and stop any resistance, we’ll cease to exist as an independent state,” , “[Putin] made it clear that he would not stop before any losses and costs in achieving his goal,” Kuchma also said he believed that such an ultimatum had been delivered not only to Ukraine, but to the whole of the Western world. (UNIAN agency in English – yesterday)

5. This still doesn’t mean that the 180 degrees turn made by Syriza looks good. It is back to normal in Western European politics – “muddle through” is the main principle. It is a bit surprising that YV has agreed to be hired to lead the effort. Maybe he will end up being a celebrity chef cooking books. Business as usual in the Eurozone.

James Schipper,

You’ve misunderstood, as usual, what Bill was saying. Its not that the new Drachma couldn’t devalue, it is that it needn’t devalue. The ND would be a completely new currency and its value would be dependent on the policies of the Greek government which introduced it.

The exact starting value isn’t important. The ND could be made to be worth 10 euro if that’s what the Greeks wanted. That wouldn’t of course mean that salaries would be transferred on a 1:1 basis.

That said, there would be no sense in the Greek government having a high exchange rate policy. They need to let their currency float. That’s what Iceland did after the 2008 crisis and they have got low unemployment and a high GDP per capita as a result. That’s the successful course of action to follow. The Greek course of action is the failed course.

We don’t need to delve into any economic theory. That’s what we see happen in practice. In science, but not in mainstream economics, practice trumps theory every time.

… forgot to add (what is relevant) that a properly designed balanced fiscal stimulus will involve spending multiplier effect. To seal off leakages into saving they can just slam a tax on bank deposits and other financial assets – and introduce creeping capital controls (somehow).

Also – the Greek govt can increase VAT on these groups of products which are predominately imported (- especially from the Teutonic Nation, such as luxury cars or submarines). There is always some room for wriggling – if there is a way to ensure staying in power for a while. What I am not so sure about.

Also …

Just watch the capital flight from Ukraine, just now, just under our noses. Of course – they are in a war. But it is pretty massive. People started panic buying of food. Google for the information or just for example go to UNIAN website (and filter out the propaganda) – it is worth watching the train wreck in slow motion.

The assumption that something similar cannot be engineered in Greece is unfortunately not true. We are not watching a gold fish in an isolated fish tank. We are watching predators and preys in a so-called highly polluted natural environment.

Incorrect – Its a private monopoly.

The bank in the modern state owns you and the commons.

Pre modern fiat kings simply produced the medium and dispensed it into the nation.

The King and the state was effectively the same unit.

When the banks seized England again the state became the crown,

A somewhat nebulous entity used by the banks to extract peoples life force.

To repeat – in a real nation the money as the ultimate expression of the commons is part of that society.

The kings face is on the coin but he does not own it.

In a modern society the banks feel they own that money and indeed they do.

They can call in that money at anytime or anywhere using the various police and tax functions of the state.

Previously Kings relied on their good name and judgement when they asked for extra tax income.

In cases where they relied on Jews to concentrate wealth and taxed them in return for protection the commerce of the nation suffered gravely.

This brutal centralisation of life was best seen in Tudor England.

The turmoil of that time is a general characteristic of the money power.

Its a very old programme.

Dear Neil and petermartin2001

The new drachma HAS to devaluate if Greece is to improve its competitive position. One problem afflicting the Greek economy is that Greece had higher inflation than most other countries in the Eurozone but could not lower the exchange rate of its currency to avoid a real upvaluation, for the obvious reason that it no longer had its own currency.

Let’s suppose that after a Grexit, everybody in Greece will be paid the same amount in drachmas as before they were receiving in euros. If the exchange rate of the drachma to the euro will remain at 1:1, then nothing will have changed with regard to Greece’s competitiveness.

Let’s assume that a Greek factory worker gets 15 euros per hour and produces 5 widgets per hour. To keep it simple, we assume that labor costs are the only costs. If the international price of widgets is 2 euros, then Greece is not competitive because it has to sell its widgets for no less than 3 euros.

If after a Grexit, the worker receives 15 drachmas and each drachma is worth 1 euro, then the Greek widget industry will remain uncompetitive. If the new exchange rate will be 1.5 drachma to 1 euro, then Greece will be competitive because it can now sell its widgets abroad for 2 euros.

Regards. James

Anyone who reads the (generally well) translated interview given by Varoufakis to Hadjinikolaou and pretends not to appreciate what the actual underlying plan is, then I am going to assume they have an agenda. one that is NOT helpful to the cause of Greece.

And, yes, as armchair analysts, we all need to take a nice big gulp of humility.

Dear GrkStav (at 2015/02/27 at 16:26)

Yes, the Finance Minister has articulated what he is doing. I am not pretending not to know that. What they are principally doing is staying in the dysfunctional Eurozone and trying to make something of that. That is my source of disagreement. It is a monetary arrangement that is anti-prosperity.

Syriza is also banking on a huge EIB injection (or similar) which I would suggest will not be forthcoming. So that is a difference based on different conjectural assumptions.

Syriza has no more intelligence on that likelihood than any well-informed observer at this stage.

best wishes

bill

They shouldn’t have to pay for the land anyway. It belongs to everyone!

“So you could suspend planning permission until you have sufficient house builders signed up to build the 500K houses at a price that is acceptable to government. Remove their alternative sources of employment until they deal.”

You could do this, if you wanted to push up land prices and restrict supply…

Also, how would you “remove their alternative sources of until they deal.”

Why would you want to do this where there is a simple solution – Land Value Taxation. People use the land or sell it. At 100% land ‘value’ is nil.

Or they could just be using an open-ended approach whereby

1. They seek to cement and build on the ‘voting’ and ‘social movement/people power’ support that brought them to office

2. they seek to begin internally transforming the architecture of the EU and EZ whilst getting SOME breathing room to effect #1 above

3. working on changing the ‘culture’ built over 40 years of ‘nudge-nudge, wink-wink’ particularistic impunity for anything other than blatant violations of the criminal code and of the civil+administrative code, primarily by the not well-connected suckers such that

4. if 2 does not succeed they can trigger the ‘nuclear’ option by the ECB which would lead to ‘exit’ from the eurozone as such whilst being in a better material and organization position to handle the transition with less disruption that would be the case at present.

To put it bluntly, bill, you and other outsiders have basically nothing riding on whether your predictions come true or not. THEY (and we, I am also a Greek citizen, practically my entire family live there, work there or are pensioners there, etc) do. You (and others) are like ‘coaching theorists’ who have never coached an actual club, have never faced the rigors and constrains of the actual job of coaching but are, nonetheless, critiquing actual coaches’ decisions, ‘calls’, practices, etc.

Dear GrkStav (at 2015/02/28 at 17:01)

In other words, you reject all journalism, research-based insights, and other commentary as being a valid form.

Only direct experience is apparently a source of knowledge in your world. We would not have made much progress if that was true.

best wishes

bill

How can Greece avoid austerity even under 0 surplus condition? It can not do it with positive surplus going to ECB forever.

Yanis proposes (and he will implement it) is to print paralel money called TAN (tax advance note), but in my opinion it is a future budget reducing mechanism whith which to pay for additional spending.

But my proposal is much more cunning and stealthy. It is using the fact that banks destroy money when clients pay off the credits. Why not give them something else to destroy instead of real money that people are giving them?

Greece can print notes that only banks accept in lieu of credit payment and give it to all greeks on monthly basis. Say 100€ worth of note to every citizen and 50 to every child.

That would be about 1 bilion a month or 7% aditional spending deficit. Since Galbraith asks for 10% deficit spending for Greece in order to get out of depression, this could help greatly.

Those without outstanding debt at banks can sell their notes to those with or open a credit line and pay of their utilities and taxes. Banks print money when issuing credit.

This would stop the need of banks for further bailouts since credit defaults stop and also accumulate banking reserves that Greece can then borrow, if it forces it’s banks to stop lending to foreign governments that almost destroyed them.

Yanis also proposes to implement USA style personal and corporate bankrupcy (same effect as printing notes) which Eurogrop accepted, but that is slow processs and it requiers funds for seting up institutions.

Then arrives increased import from increased purchase power and to fight that Greeks have to start planing on organizing the production of previously imported stuff to prevent imports and more deficits.

WRT Neil Wilson’s post above:

“”If a civil servant who is currently paid 2500 euros…. FX is as near to a perfect market as you can have.”

What happens to the interest rate at that point?